Subscribe and receive email notifications of new blog posts.

RSS Feed

RSS Feed

8

April 2026 Alabama Gulf Coast Real Estate Stats

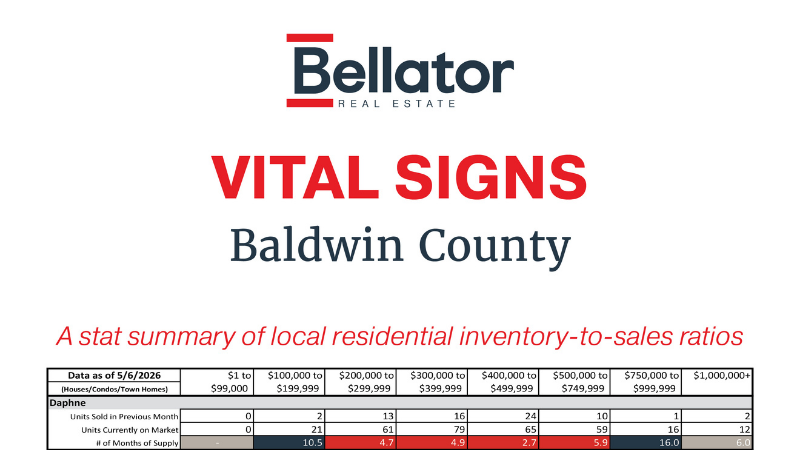

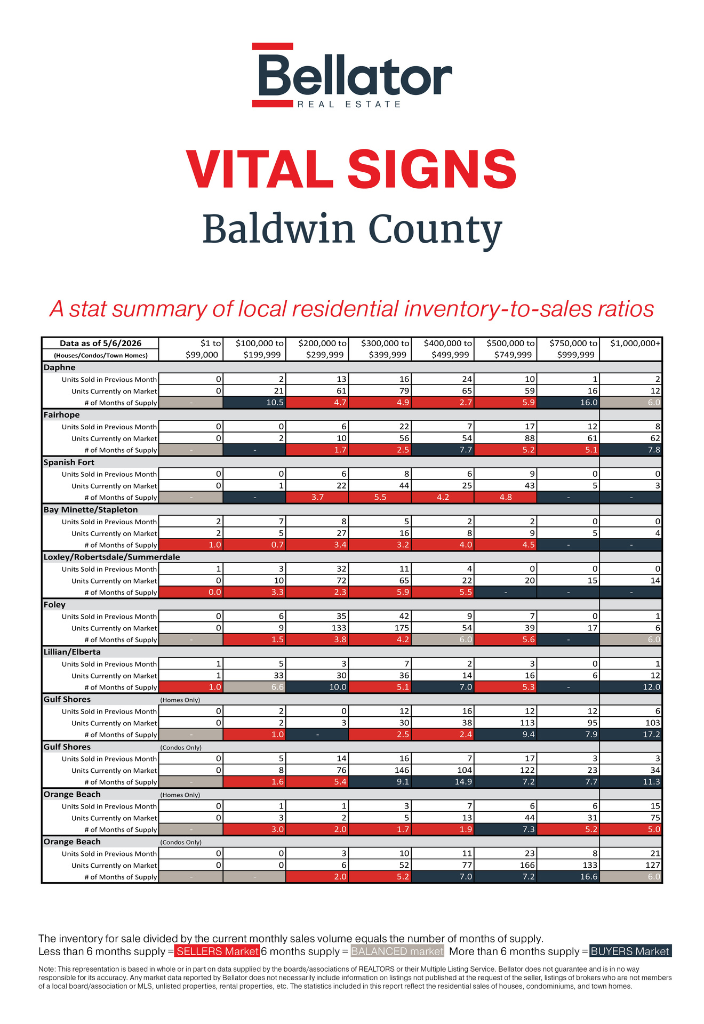

Vital Signs provides a visual representation of what's happening in the Alabama Gulf Coast real estate market. The color-coded numbers represent the absorption rate; the number of months it would take to sell every home on the market in a particular price range if no others were added. If the market is moving quickly, the absorption rate will fall below six months of supply, and if it's more of a buyer's market, it will jump above six months of supply. The rate is determined by dividing the number of units currently on the market by the number sold in the past month.

Baldwin County Real Estate Market Update

March → April 2026: Spring Market Hits Full Bloom

April brought another strong month for Baldwin County real estate, with many markets seeing increased sales activity, tighter inventory in key price points, and continued momentum in both residential and coastal segments.

If March opened the door to spring, April kicked it off the hinges.

Across the county, the story is becoming clearer:

- Mid-range homes are moving quickly

- Coastal luxury remains active

- Inventory is rising in some areas, but buyer demand is keeping pace

Let's break it down market by market.

Market Snapshot: What Changed From March to April?

Key Themes Across Baldwin County:

- Strong buyer demand continued

- Many markets remained seller-friendly under $500K

- Luxury and coastal segments saw increased activity

- Inventory expanded slightly in several areas, offering buyers more options

- Months of supply tightened dramatically in select price ranges

The spring market is officially humming like a freshly tuned outboard motor along the bay.

Area-by-Area Breakdown

Daphne: Buyers Shift Upward

Daphne remained highly active, but buyer activity shifted into higher price points.

What Changed:

- Sales in the $400K–$500K range jumped from 17 → 24

- Luxury activity improved with new $1M+ sales

- Months of supply tightened significantly in the $400K–$500K range (down to 2.7)

What Stands Out:

- Lower price ranges slowed slightly

- Inventory rose modestly, especially under $200K

Takeaway:

Daphne's move-up market is thriving, and well-priced homes in the mid-to-upper ranges continue to attract strong demand.

Fairhope: Balanced and Consistent

Fairhope continues to operate like a polished luxury boutique: steady, selective, and resilient.

Highlights:

- Strong sales in:

- $300K–$400K

- $500K–$750K

- Inventory remained relatively stable

- Months of supply improved in luxury tiers

Takeaway:

Fairhope remains one of Baldwin County's healthiest and most balanced markets, especially for upper-end buyers and sellers.

Spanish Fort: Cooling Slightly After a Hot March

Spanish Fort slowed modestly after March's surge.

Changes:

- Sales dipped in the $300K–$400K range

- Inventory held relatively steady

- Months of supply rose in some segments

Takeaway:

Still a strong market overall, but April showed signs of normalization after an exceptionally active March.

Bay Minette / Stapleton: Quietly Competitive

One of the more interesting shifts happened here.

Highlights:

- Strong increase in affordable sales activity

- Months of supply tightened sharply under $300K

- Entry-level inventory remains limited

Takeaway:

Affordable inventory is moving quickly, creating stronger seller leverage in lower price ranges.

Loxley / Robertsdale / Summerdale: Entry-Level Demand Surges

This area saw a major spike in activity.

Biggest Story:

- $200K–$300K sales exploded from 20 → 32

- Months of supply dropped to just 2.3 months

Takeaway:

This market has become one of the county's strongest affordable-home hotspots.

Foley: Strong, Stable Momentum

Foley stayed active, though at a slightly more measured pace than March.

Highlights:

- Continued strong sales in:

- $200K–$400K ranges

- Inventory expanded, especially in mid-range price points

- Supply remains relatively balanced overall

Takeaway:

Foley remains one of Baldwin County's most dependable high-volume markets heading into summer.

Lillian / Elberta: Slower but Still Tight in Places

What Changed:

- Sales cooled in several price ranges

- Months of supply rose noticeably under $300K

Takeaway:

A softer April, though inventory remains relatively constrained in select segments.

Coastal Market Spotlight

Gulf Shores

Homes:

- Strong activity continued in the $300K–$750K range

- Inventory remains elevated in luxury tiers

Condos:

- Big increase in sales activity

- Months of supply dropped sharply in several price points

Takeaway:

The condo market showed meaningful improvement, while single-family luxury inventory still creates more buyer negotiating power.

Orange Beach

Homes:

This was one of April's biggest stories.

- Massive increase in $1M+ home sales (10 → 15)

- Inventory stayed relatively stable

- Months of supply tightened significantly

Condos:

- Luxury condo activity surged

- $1M+ condo sales tripled from 7 → 21

- Mid-range condo inventory remains elevated but improving

Takeaway:

Orange Beach luxury buyers came roaring back in April. The high-end coastal market is very much alive.

Key Trends to Watch

- The Mid-Range Market Still Rules

Across Baldwin County, the $200K–$400K range continues to dominate:

- Highest sales volume

- Fastest turnover

- Tightest inventory

- Luxury Coastal Markets Are Heating Up

April showed significant movement in:

- Orange Beach luxury homes

- Gulf Shores condos

- Fairhope upper-end inventory

The second-home and lifestyle buyer appears increasingly active heading into summer.

- Inventory Is Slowly Expanding

Many markets saw modest inventory growth:

- More options for buyers

- Slightly less pressure than early spring

- But demand is still absorbing inventory quickly in key ranges

Final Thoughts

April reinforced what March first hinted at:

Baldwin County's spring market is in full stride.

- Buyers remain active

- Sellers in desirable price ranges still hold leverage

- Coastal luxury markets are regaining momentum

- Affordable inventory continues to move quickly

The market feels less frantic than the ultra-competitive years, but far healthier and more sustainable. Not a fireworks finale. More like a powerful tide steadily rolling in.

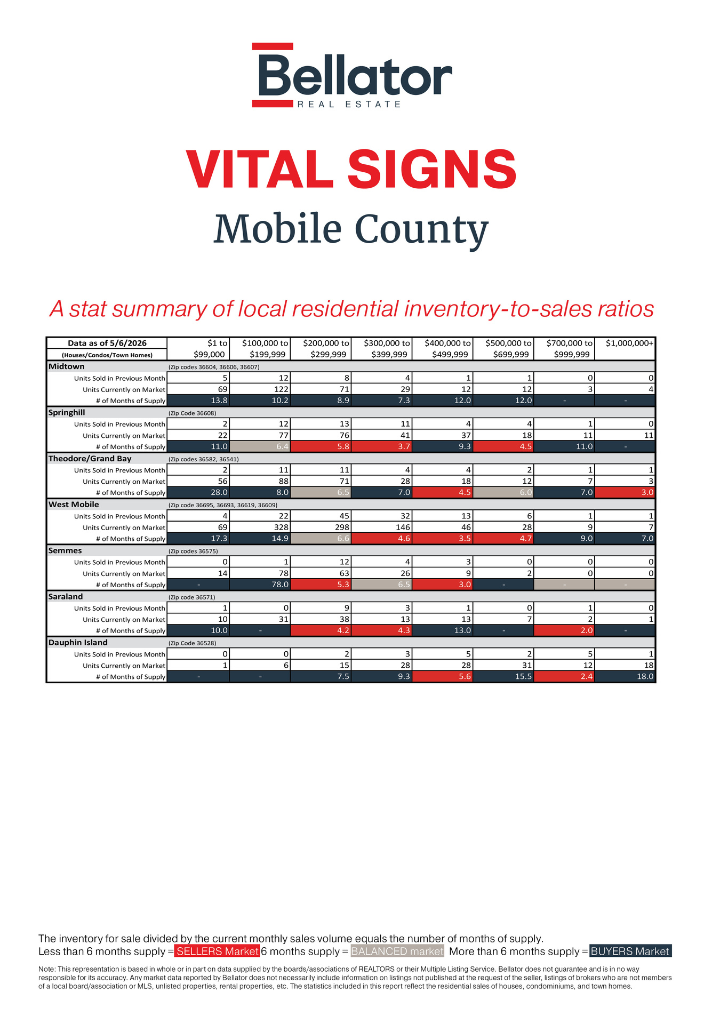

Mobile County Market Update: Comparing March vs. April 2026 Real Estate Trends

Spring has officially arrived in Mobile County's housing market, and April brought a noticeable shift in activity across several key areas. While inventory continued to climb in many markets, buyer activity also strengthened in several price ranges, especially in West Mobile, Springhill, and parts of Theodore/Grand Bay.

The result? A market that feels more active, more competitive in select segments, and increasingly price-sensitive as buyers carefully navigate rising inventory levels.

Here's a breakdown of how Mobile County performed from March to April 2026.

Overall Market Snapshot

Across Mobile County, April showed:

- Increased buyer activity in mid-range price points

- More inventory entering the market

- Improving conditions in some previously slower segments

- Continued challenges in higher-end luxury inventory absorption

- Strong momentum in West Mobile and Springhill

The $200,000 to $399,999 range remained the heartbeat of the market countywide, accounting for the majority of closed sales.

Midtown Mobile

Midtown continued to show stable demand, particularly in the $100K–$299K price ranges.

Key Changes from March to April:

- Sales in the $100K–$199K range doubled from 6 to 12 units sold

- Inventory remained relatively steady

- Months of supply improved significantly under $200K

- Higher-end inventory continued moving slowly

The $300K–$399K market cooled notably:

- Sales dropped from 15 to 4

- Months of supply increased from 1.8 to 7.3 months

Takeaway:

Affordable Midtown homes remain highly attractive to buyers, while upper-mid-tier properties experienced a slower April pace.

Springhill

Springhill posted one of the strongest overall performances in April.

Highlights:

- $300K–$399K sales jumped from 6 to 11 units

- Inventory remained balanced despite stronger activity

- Months of supply improved in nearly every major category

Particularly strong movement occurred in:

- $100K–$199K homes

- $300K–$499K homes

The luxury market above $700K remained slower but showed signs of stabilization.

Takeaway:

Springhill continues to operate as one of Mobile County's most balanced and desirable submarkets, especially for move-up buyers.

Theodore & Grand Bay

This area remained one of the county's more affordable and active regions.

Notable Trends:

- Sales under $200K increased from 9 to 11

- Inventory remained manageable

- The $400K–$499K segment strengthened considerably

However:

- The $200K–$299K segment slowed from 23 to 11 sales

- Months of supply in that category rose from 3.0 to 6.5 months

Takeaway:

Theodore and Grand Bay continue attracting value-focused buyers, though inventory growth is beginning to soften competition in some price brackets.

West Mobile

West Mobile once again led the county in overall transaction volume.

April Performance:

- 124 total sales across tracked price ranges

- Strongest activity remained in the $200K–$399K range

- $100K–$199K sales climbed from 17 to 22

- Luxury sales above $1M finally recorded activity

Inventory also increased:

- $400K–$499K inventory rose from 38 to 46 units

- $700K+ inventory expanded as well

Despite rising inventory, months of supply remained relatively healthy in core price segments.

Takeaway:

West Mobile continues to be the engine room of the Mobile County market, fueled by consistent buyer demand and broad inventory selection.

Semmes

Semmes experienced a slight cooling trend in April.

Key Observations:

- Sales under $200K declined sharply

- Inventory remained mostly flat

- The $200K–$299K range stayed relatively healthy with 12 sales

One unusual statistic:

- Months of supply hit 78 months in the $100K–$199K range due to extremely low sales volume and available inventory imbalance

Takeaway:

Semmes remains steady overall, but buyer activity became more selective in April.

Saraland

Saraland delivered a mixed month with stable activity in core price ranges.

Market Changes:

- $200K–$299K remained the strongest segment with 9 sales

- Inventory increased slightly

- Upper-end inventory above $400K expanded while sales stayed limited

The market between $200K–$399K remained the healthiest and most balanced.

Takeaway:

Saraland continues offering relatively stable market conditions, particularly for buyers seeking mid-priced homes.

Dauphin Island

Dauphin Island saw increased luxury and waterfront activity in April.

Major Trends:

- $400K–$499K sales increased from 3 to 5

- $700K–$999K sales jumped from 1 to 5

- Inventory also expanded in luxury categories

However:

- Months of supply remains elevated in most segments

- Luxury inventory continues outpacing buyer absorption overall

Takeaway:

Dauphin Island's luxury and vacation-home market showed encouraging momentum in April, though inventory levels remain high.

What This Means for Buyers and Sellers

For Buyers:

- More inventory is creating additional negotiating opportunities in many areas

- Midtown, Theodore, and West Mobile continue offering strong value

- Luxury buyers now have more options and leverage

For Sellers:

- Proper pricing is becoming increasingly important as inventory grows

- Well-presented homes in desirable price ranges are still moving quickly

- The strongest demand remains concentrated between $200K–$399K

Final Thoughts

April 2026 showed a Mobile County market steadily transitioning into a more balanced environment. While affordability-driven segments continue performing well, rising inventory levels are beginning to reshape negotiation dynamics across the county.

Areas like West Mobile and Springhill remain exceptionally active, while coastal and luxury segments are gradually finding their rhythm heading deeper into the spring season.

As always, local expertise matters more than ever in a market where conditions can vary dramatically by neighborhood, price point, and property type.

Contact your Bellator agent today to strategize your next move to the Gulf Coast.

Privacy Policy / DMCA Notice / ADA Accessibility